Overall, 2019 was another turbulent year for most shipping markets, overshadowed by preparations for the IMO 2020 sulfur regulations, rising geopolitical tensions, the trade war between the USA and China, as well as natural disasters disrupting global supply chains. This article provides insight into the changes seen in the maritime software landscape under these turbulent conditions: On a high-level, the increase of software solutions reported in the recent years seems to have flattened out in 2019.

This is partially caused by the fact that some solutions were being consolidated, but also fewer new vendors were entering the market. Venture capital investments were up from last year, but only due to one single major transaction. That said, should you as a reader conclude that the market is saturated and the willingness of investing into digital solutions will decline? No, absolutely not. We believe, now more than ever, it is important to be on the outlook for an increase in maritime digitalization efforts, since the “real world” use cases with healthy ROIs are finally starting to emerge in the market due to more mature and scalable solutions. 2020 will be the year to get started and the ones not willing to embrace the opportunities at hand, will lag behind the players that do.

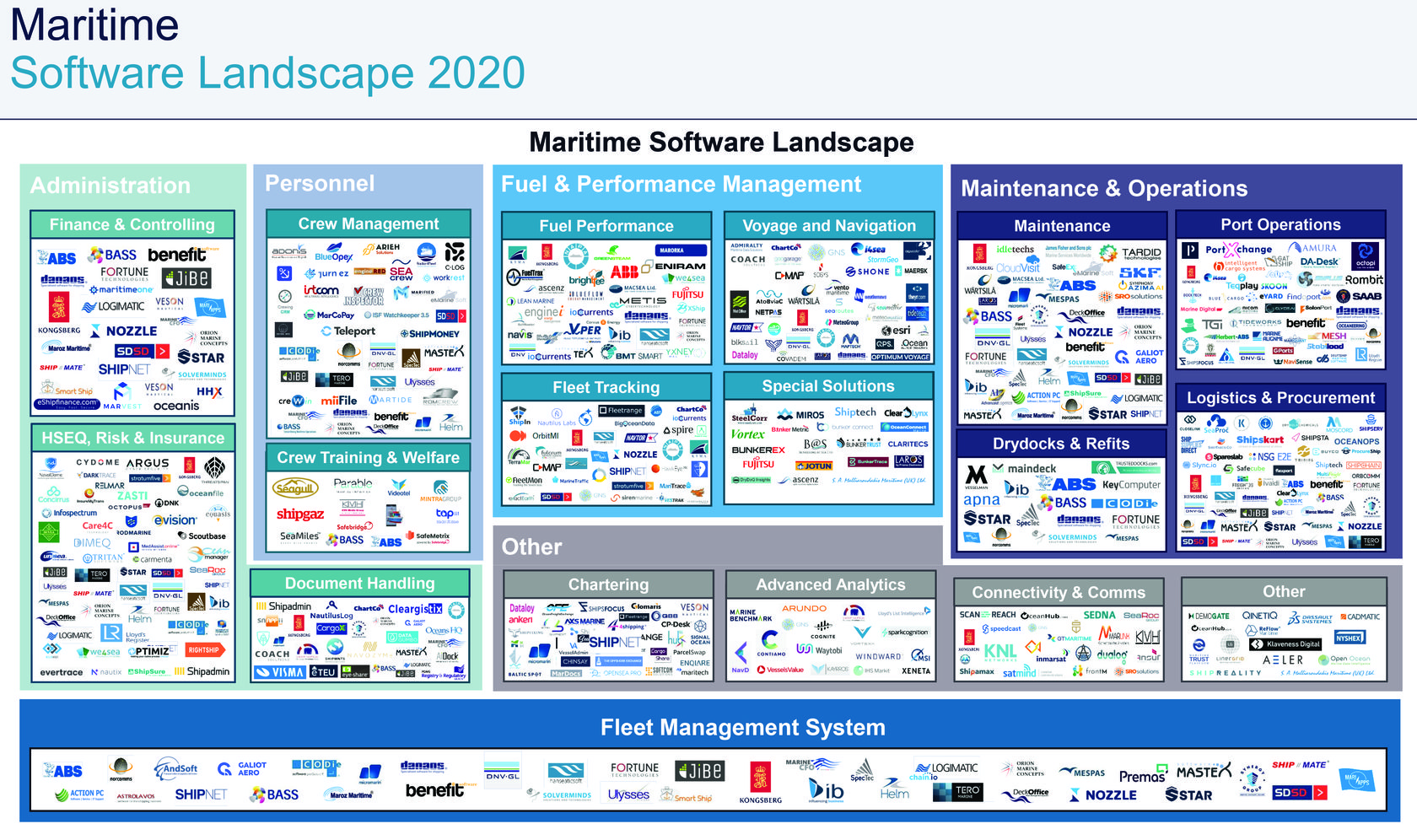

In the 2020 version of our software landscape report, we have mapped almost 500 software vendors across the maritime landscape, a number that is only slightly higher than in beginning of 2019. We have seen just a small increase in the number of new vendors entering the arena, which was partly offset by a number of consolidations across existing vendors such as for example BMT Smart being acquired by Greensteam, and ChartCo and Marine Press merging to form OneOcean.

With only 20 new vendors mapped during 2019, the last year’s increase in maritime software products is significantly lower than in the two previous years, despite 2019 being a record year of venture funding into maritime startups. In total $1.14 billion were invested; however, the lion’s share of $1 billion was dedicated to one single company only: the digital freight forwarder Flexport. The remainder being invested into maritime startups was only $140 million, which is significantly less than the previous years’ investments. The largest part of the 2019 investments went into the 4 startups Traxens (Container IoT), FreightHub (Digital Freight Forwarder), Rombit (Port Operation Efficiency) and Nautilus Labs (Fleet Management).

New vendors that joined our mapping were spread across a number of different areas, such as e.g. ship finance (Oceanis), crew management (MarCoPay, Marified, Arieh Solutions), port management (Marine Digital, PortXchange, eYard), market intelligence & analytics (Oceanbolt, NavD), Fleet Tracking (OrbitMi) and supply chain (OceanOps, Boxport). It seems that the market has finally reached a saturation in the area of fuel & energy monitoring solutions, where not many new entrants seem to be willing to challenge the well-established existing vendors. Also, we observed a continuing large growth in supply chain related vendors, as the interest of investors seems to have shifted from purely maritime startups in a narrow sense, to focus on intermodal supply chain related startups, which are often closely linked to the container shipping segments. Since these vendors are not exclusively focused on the maritime space, only the most relevant ones have been mapped out in our graphic.

What are the technology trends?

At the core of maritime software solutions remains cloud technology, which is often paired with an edge computer that is installed onboard. While the cloud enables shoreside offices to access and monitor their data almost in real-time from anywhere in the world, the edge computers onboard facilitate data capture from OT systems, help bridge potential connectivity losses, process data already onboard in order to limit bandwidth requirements as much as possible, and of course to provide insight to the onboard crew on the performance of the vessel.We also see a lot of talk on standardization of data, which is a prerequisite for collecting data from similar systems from different vendors. In the past, this has proven to be difficult, given that most installed systems were never intended to be part of something bigger than themselves. Consequently, there are often inconsistencies across different vessels even in systems from the same vendor. This is something that is addressed through solutions like Kongsberg’s Vessel Insight and similar solutions from other vendors. We strongly believe that efforts like these will be the answer to the industry’s challenge of getting access to standardized data across systems and fleets - and making it available for all types of services to build on top through well-defined and documented APIs.

Last but not least, the number of software vendors experimenting with blockchain technology is also increasing, especially in the area of document handling and document sharing, enabling e.g. a safe transfer of trusted documents, such as ship or crew certificates. So far none has taken a significant market share, but we are starting to see alliances form – which is an interesting development towards more commercially viable adopted solutions.

So what can we expect for 2020?

Given the current global turmoil in the markets, it is obviously hard to say how it will affect the market for digital services. It is, however, our opinion that the adoption of new digital services will continue to increase in 2020 as the initial shock of the impact of the Coronavirus softens.The digitalization of the maritime industry has been proceeding at an increasing pace, and, while in the beginning it was mostly pursued by larger and shipping companies, we see that increasingly also smaller shipping companies are starting to explore maritime software solutions to optimize their businesses. The somewhat slow adoption in a broad scale can probably credited to several factors, but in our opinion the three main reasons are the lack of quality data, high entry costs and lack of “real world” use-cases with healthy ROIs. That is about to change. With large parts of the older inefficient tonnage being scrapped during the last years, ship operators are now inevitably left with the task to optimize the operations of their existing fleets, and digital tools will play a key role in this. Also, the number of newbuilds equipped with additional sensors is slowly but steadily increasing – also across the less “sophisticated” shipping segments. This is indicating that ship owners have come to acknowledge the fact that they need to get ready for the digital age ahead of them.

In addition, we see that the solutions and services available to maritime players are getting more mature and it can be expected that the focus will broaden in the short term from fuel & energy management solutions - which have dominated maritime digitalization for a long time – towards other less well-established areas, such as document handling, repair & maintenance and port call optimizations.

We also expect 2020 to be a year when cyber security finally gets its deserved focus with the new IMO guidelines coming into effect on 1st of January 2021. Connecting vessels in order to get access to vessel data and sharing it with value added applications obviously also poses a risk, making it crucial to understand the exposure and take mitigating actions. The ones that will be successful will find the right balance between protecting their systems and opening them up in order to explore the business potential of digitalization.

Furthermore, we also see that “real world” use cases are starting to emerge as solutions are getting more mature and the cost of getting access to quality data is going down. Finally, some will say, as conferences and articles on maritime digitalization have tended to dive into topics and technologies already years ahead of the daily world of most ship owners in the industry. Combine that with a strengthened focus on more sustainable, efficient and greener operations, we feel confident that 2020 will be the year where the early adopters will start to reap the benefits of their investments. Are you one of them? if not, our advice to you is that it’s the time to get off the fence and explore your options. Start small, focus on proven solutions and you will be on the right track for the future.

About the Author

Vigleik Takle is Senior Vice President of Maritime Digital Solutions at Kongsberg Digital. Before joining Kongsberg Digital, he served as Chief Operating Officer in Cxense ASA, a high growth SaaS company listed on the Oslo Stock Exchange. Vigleik holds a Master of Science degree in industrial economics and technology management from the Norwegian University of Science and Technology (NTNU).About the solutions of Marine Digital

Marine Digital presents not only port management solutions (since 2019) but fuel&performance management and Catering solutions. In the spring of 2020, the development of the Catering system began and the introduction of the ship chandler company is already underway. The product Marine FOS (fuel optimization system for vessels) created in early 2020, this summer will start pilot projects with two shipping companies.Source: kongsberg.com